15 Minutes | Data valid as at the date of this article

This article does not attempt to rule out real-estate as a component and contributing asset to creating wealth. It seeks to have a realistic look at owning a home and a potential exit strategy with the view of making a profit.

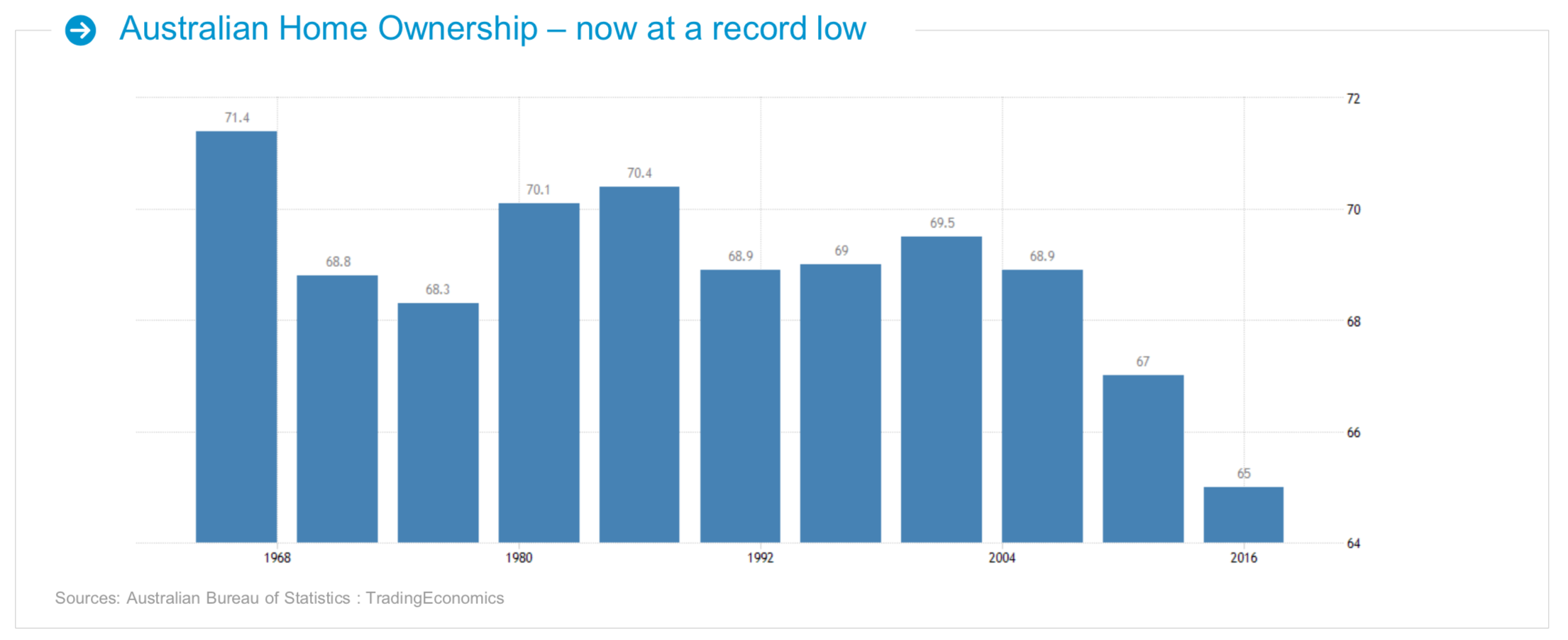

Us, as a practice and analysts are not influenced or biased by recent market corrections and down turns with residential real estate prices in Australia – that is a separate subject matter and it is in fact an exceptionally complex trajectory to determine; if we are heading for a long term downfall, stagnation or a bounce back.

If any firm, your Joe Blogg mortgage broker or really anyone claim to predict a direction for current property market in Australia; we hate to say that they have no idea what they are talking about. The best predictive analytic methods hired by RBA has not been able to point to a certain direction and we are seeing the struggle for macro policies in the making.

But for the sake of certainty and objectivity of this exercise, Let’s assume that you own the property for seven years, and that your property’s value grows nicely, at 7 per cent per year, over that time (even though there’s a prediction of a fall), and you sell in 2026 for a profit.

Many of our clients and clinicians have the inherent preference of investing in property. Because they think or their colleagues in the ward or the average financial services firm has told them

- Owning a home is the best and biggest investment.

- Buy an investment property, mortgage fees, council rates, and insurances are all tax deductible.

- Property is safe and it is brick and mortar.

- Rent money is dead money.

- Property always goes up.

- Live in it for 12 months and it will be capital gains tax free

and if you are hearing these from your accountant or your financial adviser or your bank without any research, background or substance; we think you are getting “Facebook” advice.

For the past 20+ years property investment has been a brilliant trade. Sure, there are a few leveraged-to-the-hilt investors who’ve lost their shirt trying to flip 3-bedders in QLD, but they’ve been the exception. It’s been mostly good news. But, you can’t drive a car looking out the rear window. Just because something has been a great investment, does not mean it will be.

And it is a very different story if you are an established clinician with a suite of investment properties, wanting to upgrade and move to Balwyn in Melbourne because the post code matters.

Buying a house

Let’s imagine that you’re buying a house in 2018 in Sydney. With median house prices reaching $1.15m in 2017, let’s say you nabbed a bargain at $1m, and that you managed a 20 per cent deposit – $200,000. Now you’re about to be hit with the bills. Strap in.

First, the legal fees – expect to pay around $1,800. You’ll need to pay a mortgage establishment fee ($450 on average, or package fee), valuation fee (average $200), transfer fee ($219) and mortgage registration fee ($109). Oh, and $40,768 in stamp duty. Usually likes of BoQ Specialist will flog that $100,000 as a “Good Will” loan if you don’t have the all the money and if you are locuming, because you can pay it back!

Maintaining a house

Now that you’re sorted with a property to your name, it’s just a matter of paying off the mortgage. At an average of 4.42 per cent interest, this will cost you $4016/month in (principal & interest) loan repayments. That can be tough, but it’s all you have to do?

What is often forgotten is that buildings need upkeep. One rule of thumb for calculating maintenance costs is an average of 1 per cent of the value of the property per year, so in our case, you’re looking at setting aside around $2,000 per year in order to keep the house in good repair (minimum). Then there are local government taxes and rates (averaging $775/year in NSW), home and contents insurance ($2116.58/year on average), and your ongoing mortgage fees (up to $395/year at most major banks).

Selling a house

Real estate agents’ fees are your big cost here, with NSW average commissions at 2.46 per cent plus GST – $39,360. Then there are more legal fees and a possible mortgage exit fee, depending on your mortgage type. Yep, everyone seems to get their pound of flesh or three.

So, what do you end up making?

Despite an impressive sale price, a substantial amount of “profit” is eaten up by paying over $6000 per month to maintain the asset and service the loan.

So, what do you end up taking home as profit?

Home Ownership – Cost for 7 years

| Mortgage Establishment Fee | $450 |

| Transfer Fee | $219 |

| Mortgage Registration Fee | $109 |

| Stamp Duty | $40,768 |

| Legals | $1,800 |

| Mortgage Repayments | $337,344 |

| Mortgage Annuals Fees X 7 | $2,765 |

| Building Insurance | $14,816 |

| Maintenance | $14,000 |

| Legal Fees of Selling | $2,800 |

| Agent’s Fees | $39,360 |

| Mortgage Discharge Fee | $160 |

| Total Cost | $454,591 |

Home Ownership – Profit after 7 years (assuming no tax on sale profits applies here)

| Sale Price | $1,600,000 |

| Outstanding Loan Balance | $694,999 |

| Gross Profit | $905,001 |

| Gross Profit minus costs | -$454,591 |

| Net profit | $450,410 |

Your initial $200,000 has turned into $450,410. In today’s dollars, which adjusts returns for inflation, that’s $354,018. A handsome gain of 64 per cent. This is great. But it can be bettered. Especially when you remember that none of this accounts for the time spent on maintenance and admin, the possibility of the housing market falling, or the opportunity cost of having all your money locked away.

Is there another way?

Now imagine that instead of buying a house, you use a different strategy to build wealth – starting with the same $200,000 (your home deposit) and using the same $6000 per month (your monthly costs).

In this new scenario, you invest your initial $200,000 in an investment portfolio and rent a similar house, in the same suburb. On a house worth about $1m, you’ll likely pay rent of around $3000 per month. So that frees you up to top-up your investment portfolio by an additional $3,000 a month. For seven years.

Invested in a  carefully considered and managed investment, you could end up with $530,089 after fees and “taxes”. (Again, in today’s dollars, which accounts for inflation.)

carefully considered and managed investment, you could end up with $530,089 after fees and “taxes”. (Again, in today’s dollars, which accounts for inflation.)

Of course, you should experiment with the assumptions to explore different scenarios. If property prices rise by more than 7 per cent per year, the outcome looks better for home ownership. If it falls, it looks worse.

We don’t suggest don’t buy a home to live in. But if you are relying on a single market succeeding in order to grow your wealth, speak to us – best of all, you don’t have to wait until you’ve saved $200,000 to start.

Resources

domain.com.au: Sydney median house price hits $1.15 million: Buying becoming ‘out of the question’

www.finder.com.au: The simple guide to conveyancing

finder.com.au: Home loan fees: Know what you might have to pay

finder.com.au: What is stamp duty? Free calculator and exemptions guide

realestate.com.au: Stamp Duty Calculator

canstar.com.au: How much will your mortgage really cost?

thebalance.com: How Much Should You Budget for Home Maintenance?

smh.com.au: How much your Sydney council rates will increase by in 2018

canstar.com.au: What Does Home Insurance Cost in 2017?

finder.com.au: Fixed rate home loans comparison

smh.com.au: How much your home loan repayments could rise this year – and how to stop it

abc.net.au: Real estate ‘boom is over’ as most experts tip property price weakness in 2018

openagent.com.au: Real Estate Agent Fees in NSW

canstar.com.au: Home Loan Fees You Should Know About

SQM have great property data. For Sydney rent, yields are between 2.8-3.8%. I’ve assumed ~3.6% to use round numbers for the rent.

These figures are a forecast and not a prediction. The projected balance are estimates only, the actual amounts may be higher or lower. This forecast is general information only and does not consider your circumstances.